International venture capital in Asia has flourished over the last decade, led by ecosystem platforms (“super apps”), gaming, and e-commerce. Underpinned by a list of favorable factors like large populations, a rising middle class, and increasing technological adoption, the Asia-Pacific region has become an incredibly rich market for tech investors.

By 2021, total startup deal value in the Asia-Pacific exceeded $152 billion—matching the US total in 2018 and surpassing the boom of the dot-com era. Like much of the world, the area experienced a significant fundraising decline in 2022, but it’s also likely to weather the expected global downturn in 2023 better than anywhere else in the world. China, India, and Southeast Asia, in particular, are swiftly becoming some of the most attractive venture markets in the world. However, to make the most of their investment dollars in this culturally and economically diverse region, VCs must familiarize themselves with its nuances.

As an investment consultant based in Hong Kong, I’ve been actively involved in the private investment markets in the Asia-Pacific for the last decade. One thing I would emphasize to investors targeting Chinese, Indian, and Southeast Asian markets is that although they’re geographically connected and all considered “emerging markets,” the venture opportunities in each are distinctly different. That said, as regulatory environments change and M&A-happy tech giants provide increasing competition to VC, what happens in one country can have a significant effect on markets in others. Here are the trends that I see shaping the venture environment of these markets in the coming years.

China: Tech Giants Are Supplanting VC

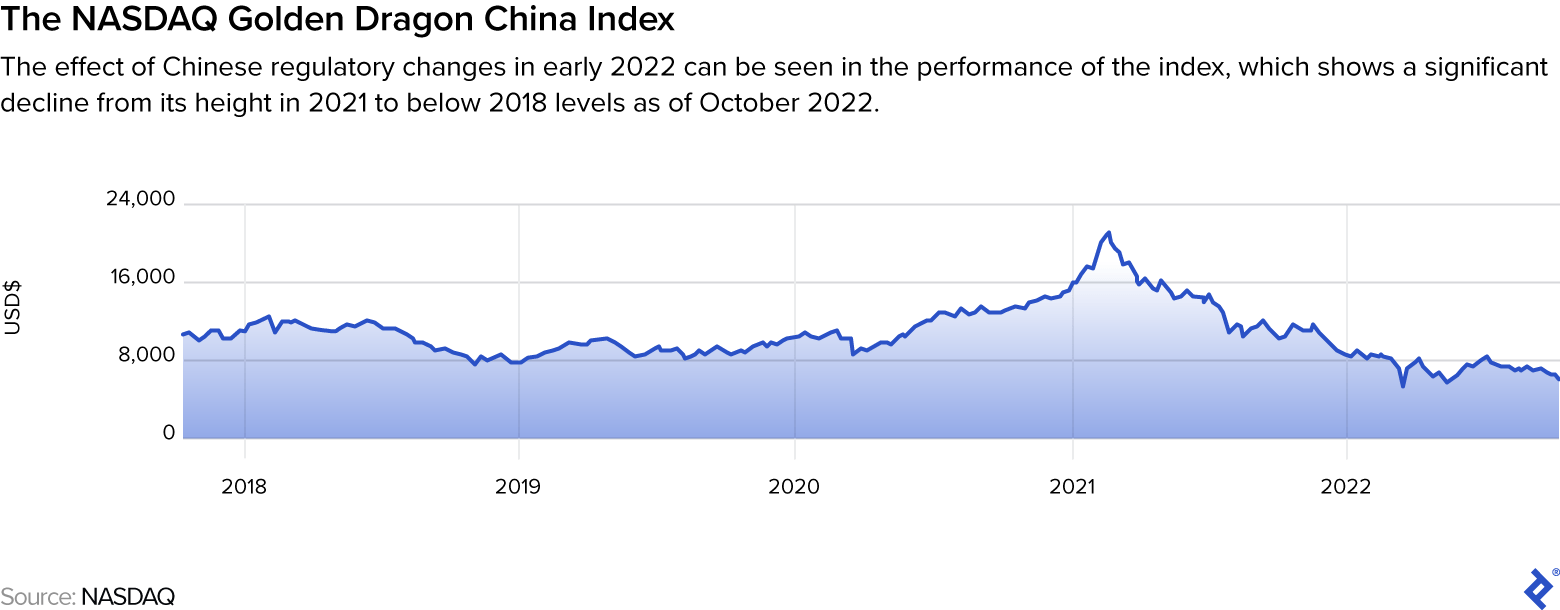

To understand the state of venture capital in Asia, you must first understand what’s happening in China, which has long been one of the most popular markets in the world for foreign VC investors. The late 1990s and early 2000s were a time of incredible opportunity for these investors as Western-educated Chinese entrepreneurs lined up a capital pipeline to boost innovation in the technology sector, ultimately building some of the country’s most formidable tech giants.

The early success stories of Japan-based SoftBank investing in Alibaba and South Africa-based Naspers investing in Tencent have since attracted more foreign VC investors looking for the next big bet, and the market continues to thrive in its maturity.

As early, foreign VC-backed tech companies gradually grew into the giants we know today, they also changed the competitive landscape of many industries in China—including the VC market itself.

China-based tech giants are now focused on building super apps. And rather than developing new products in-house, they’re instead leveraging their hefty wallets and using mergers and acquisitions to expand. This opportunistic investment strategy is now disrupting the venture investment market in the country that VC firms once dominated.

Foreign Investors Face New Obstacles

For their part, many smaller and early-stage tech companies in China have come to prefer the financial backing of domestic tech partners to funds from foreign VC firms. This kind of partnership is effectively a trusted brand’s stamp of approval for the company’s business model and thus attracts user traffic. The inclusion of the target firm’s product offerings in the acquiring firm’s broader app ecosystem also sweetens the position, as partnership opportunities increase from the additional visibility.

Foreign investors have also begun to face competition from state-backed VC funds. The Chinese government’s regulatory efforts to minimize the influence of domestic tech giants have prompted founders of new tech firms to look to these state-supported funds to help win the government’s favor and reduce burdensome oversight.

Although the Chinese government and regulators might relax the crackdown from time to time to boost the country’s economic growth, I don’t foresee a directional change in terms of its policy and initiatives toward the broader tech sector. The emphasis on taming the influence of tech giants and supporting the development of certain strategic tech sectors—including semiconductors, artificial intelligence, and electric vehicles—is not likely to be a short-term posture.

To Break Through, Offer Strategic Value

For foreign VC investors who are undaunted by these new barriers to entry and still eager to tap into the growth potential of China’s tech market, it’s essential to understand that buyers must bring more to the table than just money. Strategic positioning is key.

Does the investing firm have specific industry expertise or a focus that could give the target company access to new markets? If the target company plans to reach overseas, can the investing firm accelerate expansion?

While I was on the principal investments team of the international reinsurer Swiss Re, I led a cornerstone investment in a Chinese online healthcare company. According to recent estimates, the digital healthcare market in China is projected to reach $46 billion in 2022 and continue to grow at a compounded annual rate of 12.98%, which would mean a $84.7 billion market by 2027. In 2018, however, the sector was still in its infancy, worth only $15.2 billion. It was one of the hottest spots for growth, and competition among institutional investors was fierce.

As a foreign investor entering the mix, we were competing against Chinese and international sovereign wealth funds, Chinese state-backed investment firms, and a variety of blue-chip investors for an allocation. In the end, we tipped the deal our way by leaning into our expertise in the insurance industry. Our firm had a long history of investing in insurance and insurtech companies all over the world and could advise the target company on how to monetize its healthcare platform through partnerships with insurers.

Other deals weren’t as turnkey, so we formed a consortium or partnership to co-invest with a more strategic tech giant. In these cases, our firm had to prove how we could strategically position ourselves as a high-value partner that could benefit the China-based tech giant and combine forces to win the allocation.

For example, we wanted to invest in a Chinese startup that was also being courted by a Chinese tech giant. We were able to persuade the tech giant to let us co-invest in the startup with it by offering to support the tech giant’s overseas acquisitions in exchange.

India: A New Destination for Foreign VC

Not surprisingly, many foreign VC investors have been put off by the increasingly restrictive environment in China. A good number of them are now choosing an alternative market with similar growth prospects by actively redirecting their capital to India’s tech sector.

Among the biggest winners of this exodus are consumer-focused startups, which reached a total value of $1.6 billion in 2022. These businesses are likely to want a marketplace that is less scrutinized than China, where any app with influence on consumer behavior is closely watched. As a result, the consumer app development market in India is expected to grow at a compounded rate of 9.2% annually for at least the next four years, according to recent projections.

Further bolstering this anticipated growth in app development is the fact that India is about to overtake China as the world’s most populous country in 2023.

Overvaluation Is an Ongoing Concern

What investors need to pay attention to are the sky-high valuations resulting from too much money chasing too few deals. India’s public equity market has always traded at a premium compared to China’s, and that remains true today. Although a rich public equity market valuation does not necessarily imply a rich private market valuation, it typically acts as a comparison benchmark. With even more funding pouring into India’s tech scene, overvaluation will continue to be an issue in coming years—though recent interest rate boosts may help contain it.

Despite these concerns, there are still plenty of good reasons to invest in India’s tech sector. Many Indian tech companies, especially fintech companies like Pine Labs, Ayannah Global, Razorpay, and others, are looking to expand into Southeast Asia—something many Chinese tech giants began to do in 2015.

Whether Indian tech companies can successfully tap into the Southeast Asian market is something to watch in the next few years. If they succeed, they might be able to justify the rich valuations we see today. Otherwise, the Indian market could increasingly feel like another bubble waiting to burst.

Investors, Know Your Limits

As when dealing with Chinese firms, investors should articulate to Indian target companies the strategic value they can offer and leverage that as the grounds for price negotiation. This strategy may be impossible if you’re bidding against a large institutional investor. In that case you should be prepared to walk away if the valuation becomes unjustifiable.

That kind of calculation can feel painful in the short run, but stay focused on the long game. While at Swiss Re, I looked at a potential investment opportunity in an Indian insurtech company. Unfortunately, the target company had put us in a bidding competition with SoftBank. We calculated that matching SoftBank’s offer would wipe out our projected returns, so we called it off.

SoftBank may be paying the price for its magnanimous approach, however, as it now faces multibillion-dollar losses linked to its aggressive investment strategy. The moral? When you’re considering investing in India, discipline is crucial.

Southeast Asia: Appealing Opportunities for Secondary Investors

Southeast Asia, the third high-growth market in the region, seems to be the perfect destination for foreign investors unwilling to navigate China’s increasing insularity or India’s overheated markets.

A veritable VC desert just 15 years ago, Southeast Asia is now one of the most promising regions to invest in, with companies such as Sea Limited, Grab, GoTo Group, and others riding the super app wave to new heights. After the successful listing of a few tech companies from Southeast Asia in 2020, the trend has steadily grown, and investors are finally ready to buy into the area’s opportunities.

However, valuations in most of the region’s countries have fallen well below their listing prices, which should make investors cautious. These sluggish share price performances might be attributable to macroeconomic factors—like geopolitical risks, and interest rate hikes in the US and the EU—that have nothing to do with the company’s fundamentals. Regardless of the cause, an IPO might no longer be an attractive exit path for many VC investors in the near term.

Liquidity Events Are on the Horizon

Although IPO prospects may be poor, the next few years will see a wave of secondary investment opportunities. The earliest cohort of VC firms targeting Southeast Asia raised their funding from limited partners (LPs) between 2010 and 2015. VC funds usually have a fund life of seven to 10 years with the option to extend by a few more years upon expiration. Then, they have to return the capital to their LPs.

As a result, most of these funds will need to pursue liquidity events sometime between 2025 and 2027. If the IPO market continues to lag in this region, early-round VC funds and investors will be open to negotiating a secondary sale to private investors.

Attractive Secondary Investment Opportunities Are on the Rise

In emerging markets, secondary opportunities are appealing because investing in more mature startups can offer better risk-adjusted returns. As a secondary investor in this market, you may also find motivated sellers who will be willing to negotiate a discount on their company’s latest valuation because they are seeking a quick payout and exit.

Right before embarking on my freelancing career, I worked with the overseas investments team of Tencent, one of the Chinese tech giants that aggressively invested in the region. I was responsible for managing the group’s investments in Southeast Asia, so investors looking to exit approached me often. Many of them were willing to offer a 20% to 50% discount on the target company’s latest valuation. For unrelated reasons, we wound up not investing, and in retrospect, our choice was probably the right call. Given the ongoing correction in the share prices of the region’s tech companies since their listing, those discounted valuations most likely would have still been too high.

To Compete With Tech Giants, Offer Autonomy

Tencent, China’s Alibaba, and India tech giants like Razorpay, Moglix, and Pinelabs are more frequently competing with global VC investors for a foothold in Southeast Asia. Given their strategy to expand through acquisition, these larger cash-rich companies are often more willing to assign a heftier price tag to a target company than a foreign VC investor might be willing to pay. And existing shareholders may prefer to sell the company to these strategic investors rather than to foreign venture investors focusing primarily on financial returns.

While there are many reasons a small company might want to be acquired by a tech giant, there are also reasons it might prefer to go another route. Acquisition gives startups little choice but to align their strategy with their acquirer. Venture capital, on the other hand, can offer a company more autonomy. To avoid bidding wars with tech giants, global investors looking for early-stage opportunities in the area would be well-advised to target firms that want more control over their growth than the tech giants can offer.

Interconnected Opportunities

With the Asia-Pacific promising to be a relative bright spot during a potentially gloomy 2023, VC investors planning to become more active in the region need to understand the forces driving the state of venture capital in Asia in the next three to five years. It is critical to focus on the local factors in each market and submarket, and how each market affects the inflow and outflow of capital through the others.

Ultimately, these complexities offer not only challenges, but also meaningful opportunities to foreign VC. The variety of market forces and stages of corporate maturity across China, India, and Southeast Asia give investors the chance to hedge against volatility in some areas by balancing their portfolios in others. Doing so wisely will empower investors to capture the combined overall growth of all three.