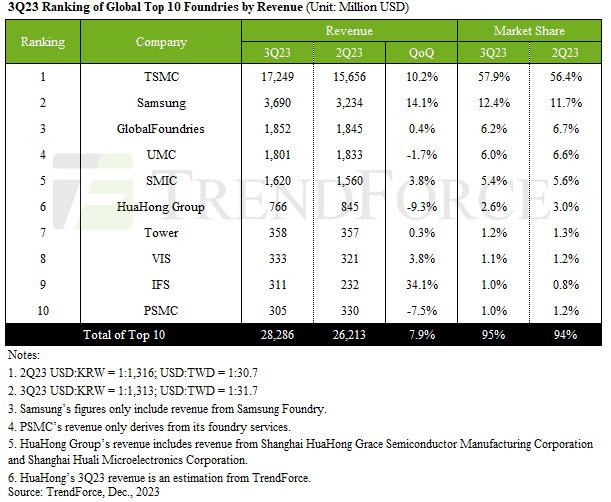

The international foundry market experienced a considerable increase in need in the 3rd quarter of 2023, according to TrendForce. The Leading 10 foundries jointly saw their income skyrocket to about $28.29 billion, marking a 7.9% boost compared to the previous quarter. Taiwan Semiconductor Production Co. (TSMC) preserved its No. 1 position as it handled to increase its deliveries, whereas Intel Foundry Solutions discovered itself in Leading 10 for the very first time in the current quarters.

TSMC, the world’s biggest foundry, published income of $17.249 billion for the 3rd quarter of calendar 2023 and protected a 57.9% foundry income market share. TrendForce thinks that TSMC’s development was supported by robust need throughout different sectors, consisting of PCs and smart devices. Among the most noteworthy chauffeurs of TSMC’s income was the official start of Apple’s 3nm chips deliveries (or rather income acknowledgment) in the 3rd quarter. With Apple’s A17 Pro smart device system-on-chip along with M3, M3 Pro, and M3 Max PC SoCs shipping in high volume, 3nm fabrication innovation represented 6% of TSMC’s overall income for the quarter, whereas sophisticated nodes represented nearly 60% of TSMC’s sales.

Samsung Foundry likewise had a rewarding quarter, experiencing a 14.1% development in its income, which totaled up to $3.69 billion, according to TrendForce. Samsung itself states that need for its sophisticated procedure innovations is increasing (which is a most likely circumstance), however TrendForce appears to be a bit more mindful as it states that development chauffeurs for Samsung varied and consisted of orders for Qualcomm’s mid-to-low variety 5G application processors, 5G modems, and time-proven 28 nm OLED screen chauffeur ICs.

GlobalFoundries preserved a constant efficiency, with its income hovering around $1.85 billion, comparable to the previous quarter. A considerable part of its income came primarily from the Web of Things (IoT) market, especially in home and commercial sectors, and considerable orders from the U.S. aerospace and defense sectors, according to TrendForce.

UMC experienced a blended quarter. Regardless of a limited quarterly income decline of 1.7%, bringing it to around $1.8 billion, the business saw a noteworthy uptick in its 28/22 nm line of product. This near 10% boost in income from these items balance out the small decrease in total wafer deliveries.

SMIC, on the other hand, taped a 3.8% boost in its income, which stood at $1.62 billion for Q3. Nevertheless, the business dealt with a shift in its customer base: income from Chinese customers rose to 84%, buoyed by the federal government’s push for localization and immediate orders for smart device elements. By contrast, income from American customers reduced due to provide chain diversity and the moving of American clients outside China. What is a bit unexpected is that although SMIC increase deliveries of Huawei’s Kirin 9000S system-on-chip (SoC) in Q3, this did not impact its income considerably. Maybe, since Chinese business bought mainly more affordable chips than their American equivalents, income from deliveries of 7nm items was balanced out by deliveries of big volumes of low-cost silicon.

What is especially notable is that Intel Foundry Solutions entered the Leading 10 foundries for the very first time in a number of quarters. IFS made $311 million in income in Q3 2023, up 34.1% quarter-over-quarter, which might be an outcome of the business’s dealing with Amazon Web Solutions, which increase production and assembly of its Graviton4 and Trainium2 system-in-packages that need sophisticated product packaging innovations.

In basic, international foundry market is on an upward trajectory, led by TSMC, Samsung, SMIC, and IFS. Smaller sized and specialized foundries– such as Tower Semiconductor and Lead International– showed blended outcomes. Tower’s earnings increased 0.3% QoQ, which is generally flat, whereas VIS published a 3.3% quarter-over-quarter boost.

By contrast, HuaHong Group experienced a 9.3% quarter-over-quarter recession, with its Q3 income being up to around $766 million. PowerChip Semiconductor Production Co. (PSMC) likewise saw its income decline by 7.5% to $305 million, mainly due to almost 10% and 20% decreases in the earnings from PMIC and power discrete items, respectively, which impacted its total efficiency, according to TrendForce.

TrendForce anticipates ongoing need as the market moves into the 4th quarter, specifically when it comes smart device elements, which is a substantial market that needs both leading-edge and relatively simplified chips.

Source: TrendForce